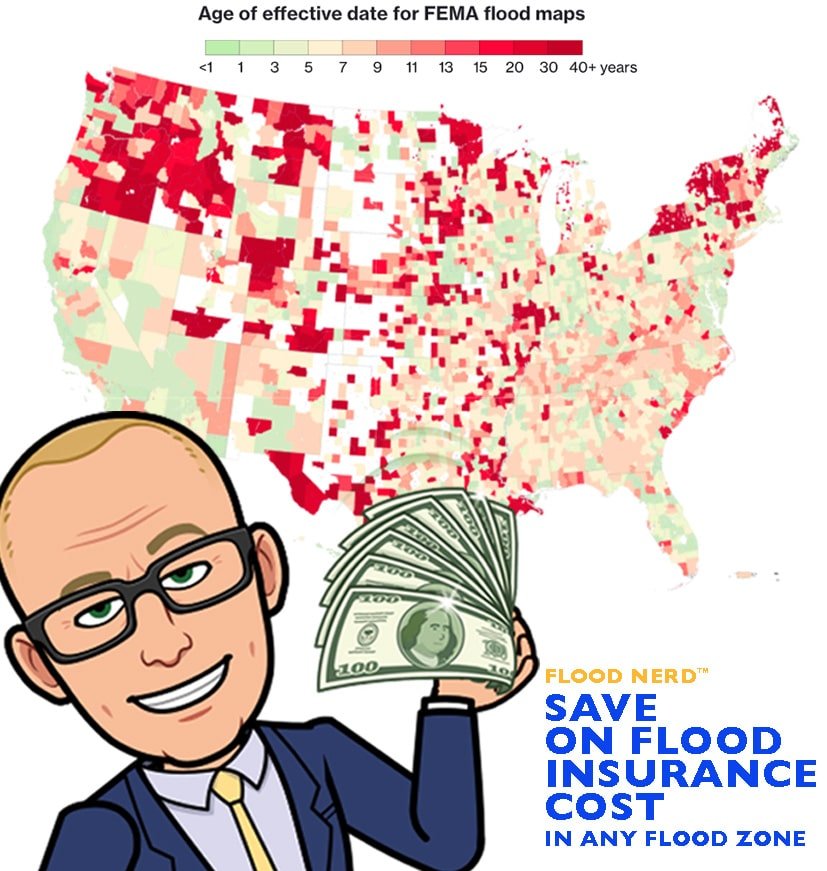

FEMA flood maps in California are often 50+ years out of date, and the landscape has drastically changed.

Run through this list. If you check even one, your risk (and premiums) could be climbing fast:

Your FEMA flood map hasn’t been updated in decades You’re near a levee, canyon, fire zone, or creek There’s been new development in your area (housing, retail, roads) You live in or near a recently burned area (risk of debris flow + flooding) Your ZIP code has elevation shifts or sits near poor drainage You’ve seen major storm runoff or street flooding near your property You’re in a “low-risk zone” but premiums are rising anyway Your current agent doesn’t specialize in flood — or only offers FEMA policies You haven’t reviewed your flood policy in over a year You’ve never priced out private flood insurance

Your FEMA flood map hasn’t been updated in decades You’re near a levee, canyon, fire zone, or creek There’s been new development in your area (housing, retail, roads) You live in or near a recently burned area (risk of debris flow + flooding) Your ZIP code has elevation shifts or sits near poor drainage You’ve seen major storm runoff or street flooding near your property You’re in a “low-risk zone” but premiums are rising anyway Your current agent doesn’t specialize in flood — or only offers FEMA policies You haven’t reviewed your flood policy in over a year You’ve never priced out private flood insurance