Five years ago, we wrote that FEMA's Risk Rating 2.0 would wash away certain flood policies and programs “like floodwaters crashing down the hillside.” That turned out to be understatement. The old map-based grandfathering, the Preferred Risk Policy program, the Mortgage Portfolio Protection Program, Submit-for-Rate — Risk Rating 2.0 took them all when it rolled out starting October 1, 2021.

But the reason we're reopening this post in 2026 isn't history. It's that the single most expensive consequence of that change is still quietly catching homeowners — usually with help from an agent who doesn't understand it. If you hold an older NFIP policy with a rate that seems too good for your property, this update might be the most valuable five minutes you spend on your insurance this year.

What is FEMA Risk Rating 2.0?

Risk Rating 2.0 is FEMA's pricing methodology for the National Flood Insurance Program, in effect since October 2021, that prices every flood policy by the individual property's address — its own elevation, distance to water, flood frequency, and rebuild cost — instead of by its flood-map zone. FEMA calls it “Equity in Action”; in practice it means no two houses pay the same rate just because they share a zone letter. (FEMA's own 2025 Risk Rating 2.0 fact sheet has the official summary, and the American Flood Coalition's five-minute explainer is a solid neutral overview.)

What Risk Rating 2.0 actually washed away

When map-based rating died, the map-based discounts died with it. The Preferred Risk Policy program went. And the old flood insurance grandfather rule — the one that let you keep rating off an older, friendlier flood map when FEMA redrew yours — stopped existing for pricing purposes. That word, “grandfathered,” is where five years of confusion (and this update) begin.

The grandfather rule after Risk Rating 2.0: what “grandfathered flood insurance” means now

Here's the part everyone got wrong, including plenty of insurance professionals: grandfathered flood insurance rates didn't vanish overnight. If you held a policy before the changeover, FEMA put you on a glide path — your premium steps up toward its full risk price a capped amount each year (18% for most primary homes). Until it gets there, you are paying less than FEMA's true price for your property. Sometimes a little less. Sometimes thousands less. That glide-path discount is what people mean today when they say their flood insurance is “grandfathered” — and the grandfathering rules that govern it are brutally simple.

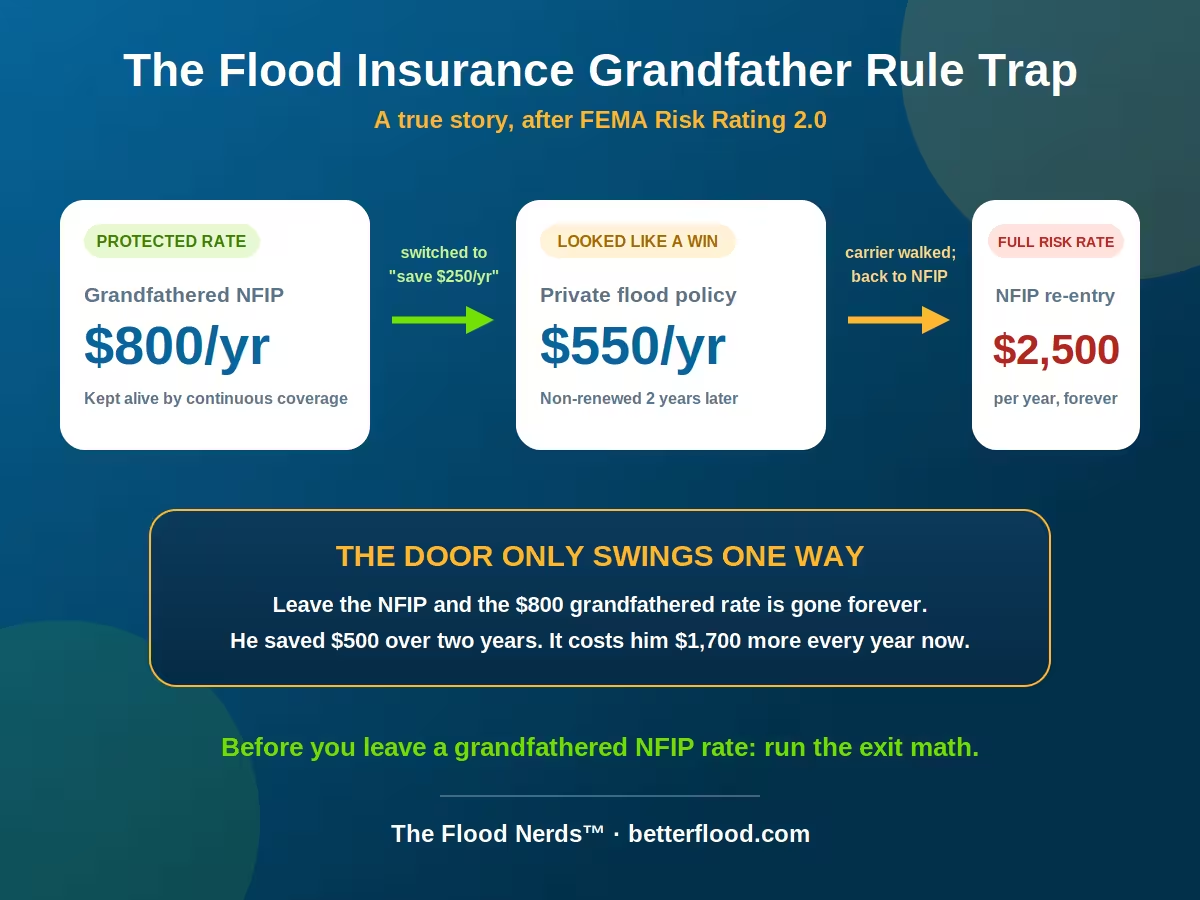

A true story: $800, then $550, then $2,500

The cautionary tale we can't stop telling

A homeowner came to us recently — not originally our client — with a story we hear too often now. He had a properly grandfathered NFIP policy on his home, paying around $800 a year. A legacy rate, protected by continuous coverage, quietly climbing its glide path but still far below his property's full risk price.

Another agent showed him a private flood policy at about $550. On paper, an easy win: same coverage, save $250 a year. He switched.

Within two years, that private carrier's underwriting appetite changed — and they non-renewed him. Not for anything he did. Carriers adjust their books; it's how the private market works. Now he needed coverage again, and the NFIP was happy to have him back — at his property's full risk rate: about $2,500 a year. The $800 rate was gone forever the day he left. And because his property had a recent flood loss on its record, the private market that had once courted him at $550 now had very little to offer at all.

He saved roughly $500 over two years. It will cost him about $1,700 more, every year, indefinitely.

Why this is resurfacing in 2026

Two forces are colliding right now. First, the glide path keeps climbing — every renewal, legacy policyholders watch their NFIP premium step up and get more tempted to shop. Second, private flood carriers keep adjusting their appetite — after the storm seasons Florida, Louisiana, and the Gulf have had, non-renewals and market exits are a normal part of the cycle. More tempted switchers, more carrier turnover: the trap has never been busier.

And to be clear about what we are not saying: we are not anti-private-flood. We place private policies every single day — for properties over the NFIP's $250,000 cap, for owners who need replacement-cost contents or living-expense coverage the NFIP doesn't offer, and yes, for plenty of homes where private simply prices better and there's no legacy rate at stake. The private market is one of the best things to happen to flood insurance. The point is narrower and sharper: if you hold a legacy NFIP rate, leaving it is an irreversible financial decision — and it deserves the same care as any other irreversible financial decision.

Before you leave the NFIP for a cheaper quote: the exit-math checklist

- Get today's full-risk number first. Ask: “If I ever came back to the NFIP, what would this property pay?” That number — not your current premium — is what you're risking. If it's triple your legacy rate, a $250/year saving is a bad trade.

- Ask how the discount you'd forfeit works. Legacy rates survive only on continuous coverage — and can transfer to a buyer when you sell. Walking away doesn't just raise your future premium; it can remove a selling point from your house.

- Weigh the carrier's staying power. How long has this carrier written flood in your state? Private flood is still a young market, and non-renewal after a bad storm year is normal behavior, not bad luck.

- Factor your claims history — and your future one. A flood loss while you're in the private market can shrink your options exactly when you need them, as it did in the story above.

- Run the five-year math, not the one-year math. Savings × years of savings, versus (full risk rate − legacy rate) × every year after a forced return. If the second number dwarfs the first, you have your answer.

What survived, for the record

Since the original post catalogued the casualties, here's the 2026 scorecard. Gone: map-based grandfathering for rating, Preferred Risk Policies, the Mortgage Portfolio Protection Program, Submit-for-Rate. Still here: the NFIP itself (reauthorized again and again, most recently with a deadline of September 30, 2026), the $250,000/$100,000 residential coverage caps, the 30-day waiting period (waived for loan-connected purchases), and Community Rating System discounts of 5–45% in participating communities. And the glide path itself survives — which is exactly why the legacy rates it protects are worth protecting in return.

Want the deeper background? Our original series covered what Risk Rating 2.0 changed and why it matters and what happened to coverage limits.

Holding a legacy NFIP rate and staring at a cheaper private quote? Send us both — before you switch. A real Flood Nerd will run the exit math, pull your property's full-risk number, and tell you straight whether the switch is a win or a trap. If your quote is right, we'll tell you that too.

Have a Nerd Run the Exit Math ➤